Our June blog focused on the general topic of future health care costs, and it got me thinking: As you transition into retirement, managing your healthcare costs becomes just as crucial as managing your investment portfolio. One of the most common surprises my clients encounter when they enroll in Medicare is a little acronym with a big financial impact: IRMAA – the Income-Related Monthly Adjustment Amount.

So here's a "bonus blog" – a simplified breakdown of what IRMAA is, how it functions, and how we can plan for it.

A General Overview of IRMAA

In simple terms, IRMAA is a surcharge added to your standard Medicare Part B (medical insurance) and Part D (prescription drug coverage) premiums if your income exceeds certain thresholds.

Unlike Medicare Part A, which is generally free if you’ve paid Medicare taxes during your working years, Parts B and D require monthly premiums. For most Americans, the standard Part B premium is a set baseline amount. However, if the Social Security Administration (SSA) determines your income is higher than the designated threshold, you will be required to pay an additional amount — the IRMAA surcharge.

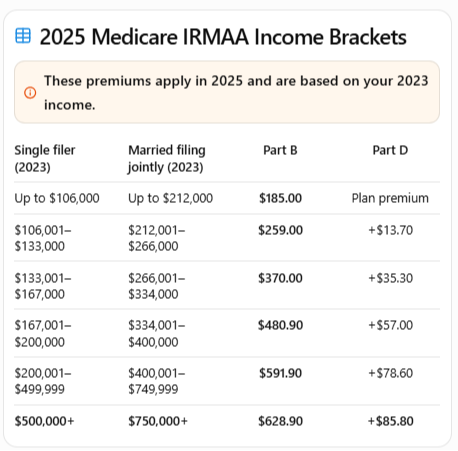

The most critical item to understand about IRMAA is that it operates on a two-year lag. The SSA calculates your surcharge based on your Modified Adjusted Gross Income (MAGI) from your tax returns two years prior. For example, your 2025 Medicare premiums are determined by the income you reported on your 2023 tax return. To give you an idea of the current numbers, for 2025, individuals with a 2023 MAGI of $106,000 or less (and married couples filing jointly at $212,000 or less) pay the standard Part B premium. (See the chart below)

Once you cross those thresholds, the surcharges begin.

How IRMAA Impacts Your Retirement Strategy

At Everest Financial, Inc., we often see the "IRMAA cliff" catch retirees off guard. Because the surcharge is based on fixed income brackets, earning even one dollar over a threshold can bump you into the next tier, significantly increasing your monthly healthcare costs.

These income thresholds are adjusted annually for inflation. If you are a high earner or have had an unusually high-income year — from selling a business, recognizing a large capital gain, or executing a significant Roth conversion — you might suddenly find your Medicare premiums doubling. This is why tax planning and retirement income planning should go hand in hand. A sudden spike in income doesn't just increase your income tax bill today, it quietly inflates your healthcare expenses two years down the line.

Strategies to Manage or Reduce IRMAA Surcharges

Fortunately, you don't have to navigate these waters blindly. There are proactive strategies we use to help manage or mitigate the impact of IRMAA:

Tax-Efficient Income Routing: We can evaluate where your retirement income is coming from. Taking distributions from a Roth IRA or a Health Savings Account (HSA) does not increase your MAGI, meaning it won't trigger an IRMAA surcharge.

Strategic Roth Conversions: If you haven't reached Medicare age yet, we might consider executing Roth conversions now. Paying the taxes today can lower your future Required Minimum Distributions (RMDs), keeping your MAGI lower when you are actually enrolled in Medicare.

Appealing the Surcharge: If your income has decreased due to a "life-changing event"—such as retirement, divorce, the death of a spouse, or a work stoppage—you don't have to wait two years for the SSA to catch up. You can file Form SSA-44 to request a new initial determination and have your premiums lowered immediately to reflect your current reality.

At Everest Financial, we believe you should be thriving in retirement, not just surviving. We’d love to sit down to discuss the potential impact of IRMAA or any other retirement planning and wealth management needs you might have.

Joseph Duffey, CLU®, RICP®, NSSA

President/Financial Advisor, Everest Financial Inc.

305 Artillery Park Drive, Suite 202

Fort Mitchell, KY 41017

(859) 291-9290

SOURCE: https://triagecancer.org/medicare-irmaa, generated via artificial intelligence.